Simple money tips. Real wealth results.

Most people fail at budgeting because their system is too complicated. Too many categories, too much tracking, too easy to quit.

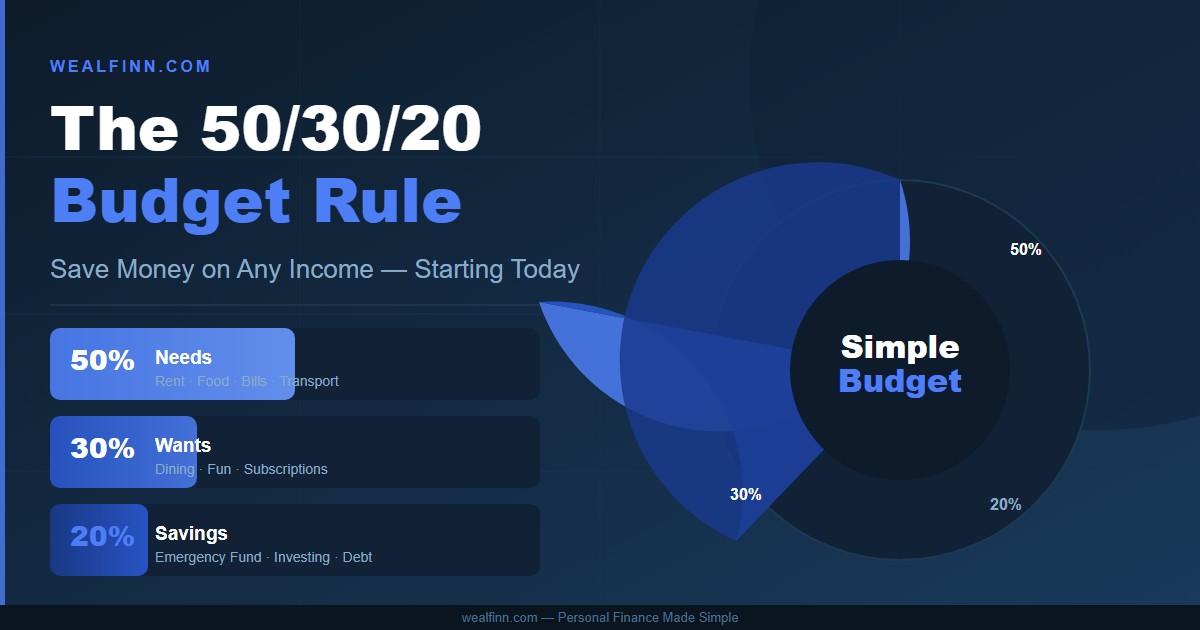

The 50/30/20 budget rule fixes that. It’s the simplest budgeting method that actually works — and you can set it up in under 10 minutes, on any income.

What Is the 50/30/20 Rule?

The 50/30/20 rule divides your after-tax income into three categories:

- 50% goes to Needs

- 30% goes to Wants

- 20% goes to Savings and debt

That’s three buckets. No tracking every coffee. No spreadsheet with 20 rows. Just three numbers to remember.

The rule was popularised by U.S. Senator Elizabeth Warren in her book All Your Worth. Decades later, it’s still one of the most recommended budgeting frameworks in personal finance — because it works.

Breaking Down Each Category

50% — Needs

Needs are non-negotiable expenses. If you stop paying them, serious consequences follow.

- Rent or mortgage

- Utilities — electricity, water, internet

- Groceries

- Transportation — car payment, gas, transit

- Minimum debt payments

- Health insurance

Notice what’s NOT on this list: dining out, subscriptions, gym memberships. Those are wants, not needs.

If your needs eat up more than 50% of your income, you have two options: increase your income or cut your biggest fixed cost — usually rent or a car payment.

30% — Wants

Wants are the things that make life enjoyable but aren’t required to survive. This is where most people silently overspend.

- Dining out and takeout

- Netflix, Spotify, and other subscriptions

- New clothes beyond the basics

- Gym memberships

- Hobbies and entertainment

- Travel and vacations

The 30% category isn’t about guilt. It’s permission — spend up to 30% on things you enjoy. Just stop at 30%.

The goal isn’t to cut out fun. It’s to know how much fun you can afford.

20% — Savings and Debt

This is the category that builds your future. Every dollar here is working for you, not just keeping the lights on.

- Emergency fund

- Retirement savings — Roth IRA, 401(k)

- Extra debt payments above the minimum

- Investment contributions

- Saving for a specific goal — house, car, travel

Prioritise in this order: emergency fund first, then high-interest debt, then retirement, then investing.

Real Example: $3,500 Monthly Take-Home

| Category | % | Amount | Examples |

|---|---|---|---|

| Needs | 50% | $1,750 | Rent, groceries, transport, insurance |

| Wants | 30% | $1,050 | Dining, Netflix, hobbies, clothes |

| Savings/Debt | 20% | $700 | Emergency fund, IRA, extra debt payments |

On $3,500/month, you’d save $700 every single month. That’s $8,400 per year — just by following three numbers.

How to Set It Up in 3 Steps

Step 1: Find Your After-Tax Income

Look at what actually lands in your bank account each month — not your salary before taxes. If your income varies month to month, take the average of your last three months and use that as your baseline.

Step 2: Calculate Your Three Numbers

Multiply your take-home pay by 0.50, 0.30, and 0.20. Write these three limits down somewhere visible — phone notes, a sticky note on your desk, anywhere you’ll see it regularly.

Step 3: Automate the 20%

Set up an automatic transfer to your savings account on the same day you get paid. This is the most important step. When the money moves automatically, you never have to rely on willpower. You spend what’s left — and what’s left is already the correct amount.

What If My Numbers Don’t Fit Perfectly?

The 50/30/20 rule is a starting framework, not a rigid law. Life isn’t perfectly divided into three equal categories.

If you live in a high-cost-of-living city, your needs might be 60%. If you’re aggressively paying off student loans, your savings category might be 30% and wants might be 10%. That’s fine. Adjust the percentages to fit your real situation.

What matters is that you have a system. Most people have no clear idea where their money goes each month. The 50/30/20 rule solves that in one afternoon and keeps it solved for years.

Key Takeaways

- 50% of after-tax income goes to needs — rent, food, transport, insurance

- 30% goes to wants — dining, subscriptions, fun, hobbies

- 20% goes to savings and debt repayment

- Automate the 20% on payday so it happens without thinking

- Adjust percentages to fit your life — the system matters more than the exact split

Once your budget is in place, the next step is building your financial safety net. Read our guide on how to build an emergency fund — it’s the first thing your 20% savings should fund.

Have questions about budgeting on a tight income? Send me a message — I read every one.