Simple money tips. Real wealth results.

Life is unpredictable. Your car breaks down. You lose your job. A medical bill shows up out of nowhere. Without an emergency fund, any one of these events can send you into debt — fast.

An emergency fund is the single most important financial safety net you can build. And you don’t need to be rich to start one.

What Is an Emergency Fund?

An emergency fund is money set aside specifically for unexpected expenses — not vacations, not new shoes, not a sale on Amazon. It exists for true emergencies only.

Without an emergency fund, one bad day can turn into years of debt. With one, it’s just an inconvenience.

How Much Do You Actually Need?

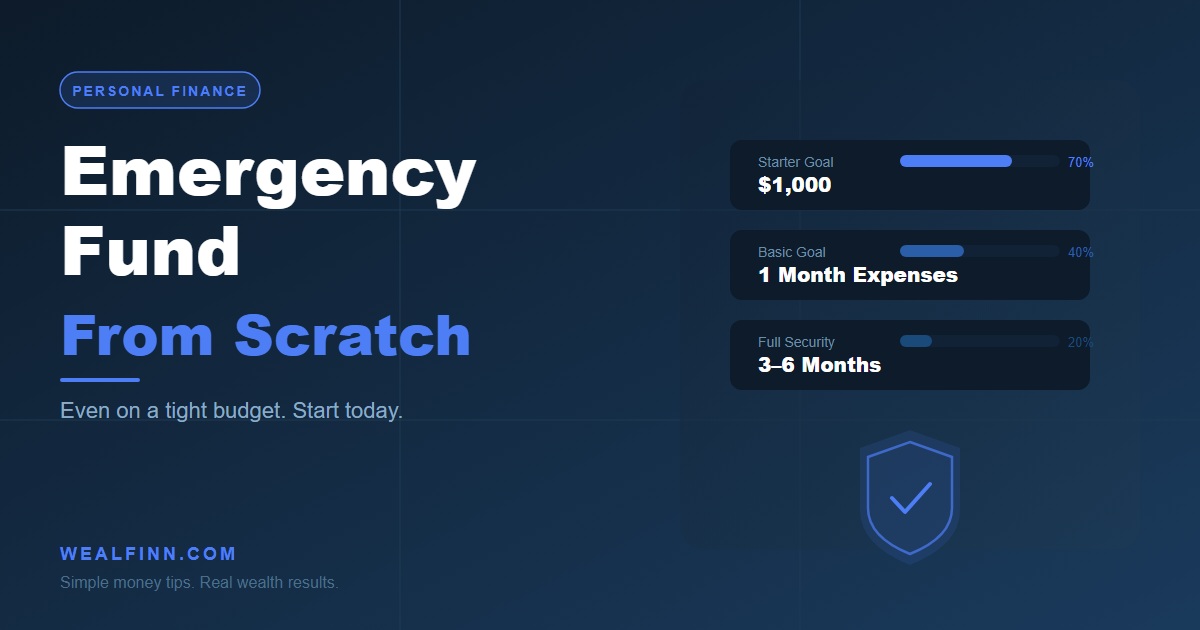

The standard advice is 3–6 months of living expenses. But if you’re just starting out, forget that number — it’s overwhelming. Here’s a simpler breakdown:

| Stage | Goal | Who It’s For |

|---|---|---|

| Starter | $500 – $1,000 | Anyone starting from zero |

| Basic | 1 month of expenses | People with stable income |

| Full | 3–6 months of expenses | Long-term financial security |

| Advanced | 6–12 months | Self-employed or variable income |

Start with $1,000. That single goal will protect you from most common emergencies.

Step 1: Open a Separate High-Yield Savings Account

Never keep your emergency fund in your regular checking account — you’ll spend it. Open a separate high-yield savings account (HYSA) where the money earns interest and is slightly harder to access on impulse.

Top options in 2026:

- Marcus by Goldman Sachs — no fees, high APY

- Ally Bank — easy transfers, solid interest rate

- SoFi — bonus interest with direct deposit

- Discover Online Savings — reliable and trusted

Step 2: Set a Monthly Savings Target

You don’t need to save hundreds at once. Pick an amount you can commit to every single month — no matter what.

Saving $50/month consistently beats saving $500 once and never again. Consistency wins.

- Tight budget? Start with $25/month

- Average budget? Try $100–$200/month

- Extra income? Push for $300–$500/month

Step 3: Automate Your Savings

Set up an automatic transfer from your checking to your HYSA on payday — before you have a chance to spend it. This is the single most effective trick to build savings without thinking about it.

Most banks let you schedule this in under 2 minutes. Do it today.

Step 4: Find Extra Money to Boost Your Fund

Speed up your progress by finding extra cash to put in:

- Tax refunds → emergency fund first

- Sell unused items on Facebook Marketplace or eBay

- Cut one subscription you forgot about

- Pick up one extra shift or side gig for a month

- Put any cash gifts or bonuses straight in

What Counts as an Emergency?

This is where people go wrong. Your emergency fund is NOT for:

- Sales and deals

- Vacations

- New clothes or gadgets

- Eating out

It IS for:

- Job loss

- Medical bills

- Car or home repairs

- Emergency travel (family illness, etc.)

Key Takeaways

- Start with a $1,000 goal — not 6 months

- Keep it in a high-yield savings account, not your checking

- Automate a fixed transfer every payday

- Only touch it for true emergencies

- Rebuild immediately after using it

Once your emergency fund is in place, you’ll be ready to start building real wealth. Check out our guide on how to start investing with $100 — that’s your next step.

Have questions? Send me a message — I read every one.